In a well-balanced portfolio, allocation to debt is crucial for capital preservation and consistent income. It acts as a cushion against risks emanating from volatile equity markets and provides liquidity for short-term needs. However, high net-worth investors (HNIs) often end up with very low returns from traditional debt products due to their subdued gross yield and being a part of the highest tax paying bracket in the country. In such a scenario, which fixed-income products should HNIs consider to earn a higher yield?

Traditional products

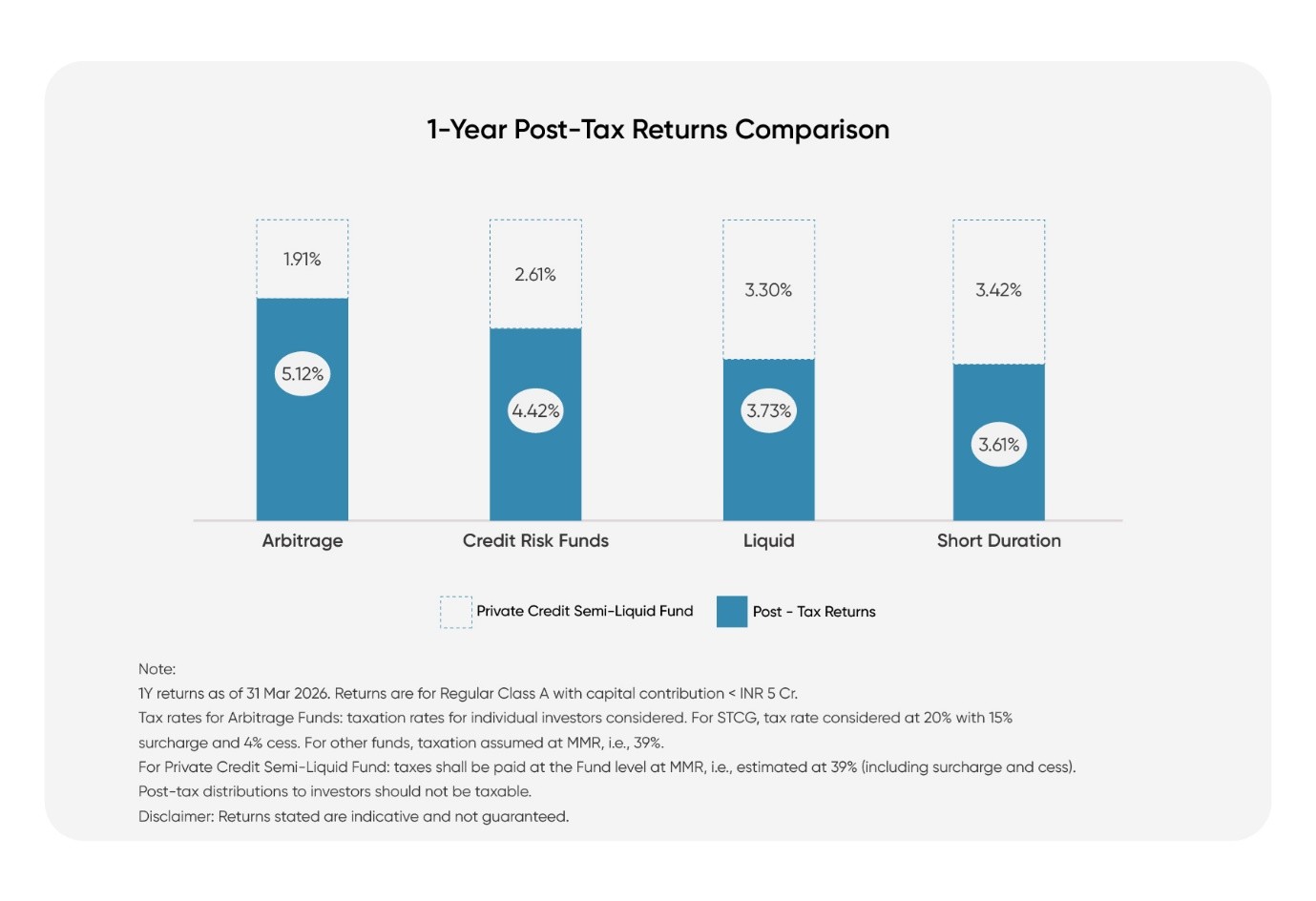

The traditional fixed-income products in debt allocation can include fixed deposits, government securities, commercial papers, etc., or indirect exposure to debt instruments via different types of debt funds. However, it is noticed that returns from such products are often very low on a post-tax basis (in the range of ~3% to 5%) as illustrated below.

Non-convertible debentures

Due to negligible returns from traditional debt products on a post-tax basis, investors seeking higher yield can look into direct investment in non-convertible debentures (NCDs)/corporate bonds. NCDs could be a lucrative choice for investors to earn higher returns; however, they come with their own demerits.

Direct subscription to single bonds is easier in public markets, whereby the issuer is higher rated (in the bracket of AA to AAA), information is publicly accessible, and the average default rate is near zero. Investors can enjoy higher yields if they invest in A and lower-rated bonds compared to the AAA and AA segments of issuers.

However, investing in the A to BBB (or unrated) segment requires close monitoring and strict due diligence due to higher credit risk compared to the AA and AAA segments. Therefore, taking direct exposure to such corporate bonds could lead to high concentration risks and potential losses due to defaults. Hence, it would make sense to invest in fixed-income products with a diversified portfolio generating higher risk-adjusted returns and having an added feature of periodic redemptions. One may look at Semi-liquid alternative investment funds (AIFs) in the private credit space for such attributes.

Semi-liquid private credit AIFs

Over the past decade, private credit AIFs have evolved from a niche concept into a preferred investment vehicle for high-net-worth individuals, institutions, and family offices. What distinguishes them is their ability to generate high-risk-adjusted returns due to their low correlation to public markets and a diversified pool of assets. Their portfolio doesn’t need to be marked to market every day.

However, many investors seeking a high-yield investment vehicle hesitate to invest in a close-ended private credit AIFs due to longer lock-in requirements This is where semi-liquid funds step in!

Semi-liquid funds in a private credit space are structured as open-ended vehicles (as Category III AIF), suited to investors looking for flexibility to subscribe and redeem at regular intervals. Along with periodic liquidity, they enable investors to earn a portfolio yield of 13-14% at a gross level and 7-7.5% on a post-tax, post-fee basis, which is gross yields for most traditional fixed income products offering liquidity. In other words, they could generate net returns that are up to ~350 basis points higher than post-tax returns from traditional debt products.

The following chart depicts the alpha on a post-tax basis generated by a private credit semi-liquid fund over and above Credit Risk, Arbitrage, and other mutual funds.

Secondly, semi-liquid funds provide investors with access to a global practice that is estimated to have cumulative assets under management (AUM) of ~US$1 trillion globally. (Notably, credit strategies dominate the semi-liquid funds in the US, comprising ~64% of the overall AUM under interval funds). Investors keen on accessing the private credit market with an exit/liquidity option can also invest in these funds with a lower ticket size (below INR 1 crore) via the Securities and Exchange Board of India (SEBI)’s Accredited Investors framework.

Thirdly, being a private credit vehicle, semi-liquid funds take exposure to multiple entities across diversified sectors, thereby significantly reducing concentration risks and potential losses from defaults. It can provide the option to receive regular income or allow compounding of income at the discretion of the investor. Also, these funds don’t follow a drawdown structure, which ensures full investment for investors in private credit markets, removing the scope for opportunity losses due to multiple capital calls.

To summarize, semi-liquid funds provide a stepping-stone for investors who are looking to invest in the private credit market but are reluctant to do so due to the lack of interim liquidity. It bridges the gap between high-yield, illiquid, and low-yield, liquid investment options and democratize the private credit market by providing investors with an option to exit at their discretion.

Disclaimer: The information provided in this article is for general informational purposes only and is not an investment, financial, legal or tax advice. While every effort has been made to ensure the accuracy and reliability of the content, the author or publisher does not guarantee the completeness, accuracy, or timeliness of the information. Readers are advised to verify any information before making decisions based on it. The opinions expressed are solely those of the author and do not necessarily reflect the views or opinions of any organization or entity mentioned.